The tax season has terms and conditions that are hard to understand and are expressed in similar ways, yet carry very different things in terms of your wallet. Tax deductions and tax credits are two terms that are often used interchangeably by taxpayers. Both cut down on what you pay the IRS, but they do it in entirely different ways – and the difference between them can have you paying a lot more. In the comparison of tax reduction vs tax savings strategies, understanding what tax benefits you are eligible to receive and their effects on your bottom line will assist you in making smarter financial decisions during the year.

What is the major difference between a tax deduction and a tax credit?

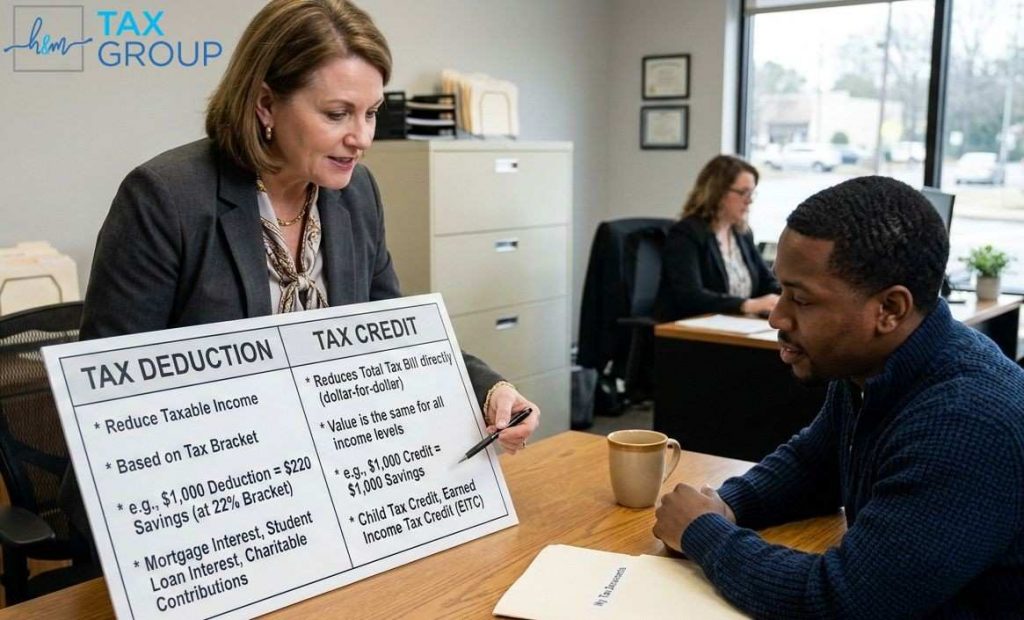

The inherent distinction between tax deductions and tax credits is in the fact that both will lower your tax bill. The tax deductions reduce the amount of your taxable income, which is the figure that the IRS uses to determine what you are liable to pay. Tax credits take away the real duty, on a dollar-to-dollar basis. Consider the following: a deduction saves you the amount that the IRS will take into account in the computation of your taxes, and a credit saves you the overall tax bill. E.g., a deduction of $1,000 may save you $220 in taxes in the 22% tax bracket, but a credit of $1,000 saves you the entire amount. This is why knowing about this tax benefits comparison will help you to see what tax-saving opportunities will add the most value to your particular financial case.

The Direct Reduction of Taxes through credits.

- Dollar-for-dollar deduction: Each dollar of tax credit saves you one dollar of your final tax bill.

- Used after calculation: Credits are used to take a deduction on taxes once you have established your total tax liability on taxable income.

- Immediate effect: A credit of 2000 is going to decrease your tax obligation by 2000 dollars, no matter which tax bracket you are in.

- More valuable: Credits usually provide greater tax reduction than an equivalent deduction.

- Direct tax relief: Credits provide simple, foreseeable tax relief, which is easy to determine and comprehend.

What are the advantages of tax deductions?

The tax deductions decrease your taxable income prior to the onset of the calculation of taxes, which indirectly reduces what you are expected to pay. When you make a $60,000 and take a deduction of $10,000, the tax paid to the IRS will be reduced to $ 50,000.

The real tax cut will be determined by your tax bracket – the rate at which your taxable income is charged. A person in the 22% bracket will save 2,200 on a deduction of $10,000 (22% percent of $10,000 = $2,200), and a person in the 12 % percent bracket will save $1200 on the same deduction. Such a comparison illustrates why deductions offer variable savings at different levels of income, as compared to credits that do not offer variable savings at different levels of income but offer a dollar-to-dollar cut at all tax levels.

What is the reason tax credits usually become better than deductions?

Tax credits are usually more substantial than tax deductions since they will directly decrease your tax bill, and not just decrease taxable income. Credits generally yield better outcomes than deductions. A credit of one thousand saves you one thousand dollars, and a deduction of one thousand only saves you between 120 and 370 dollars, depending on your tax bracket. This is because credits are particularly treasured by the middle and low-income taxpayers who do not enjoy the deductions as they have lower percentages in the tax bracket. Credits provide a large amount of tax relief that is predictable, irrespective of the income level. The professional tax advisors at H&M Tax Group assist the Dallas client in identifying and claiming all available tax credits to maximize tax savings through strategic tax planning and a thorough understanding of contemporary tax law.

Refundable and Nonrefundable Credits.

- Refundable credits: These can reduce your tax liability below zero, resulting in a refund even if you owed no taxes – such as having an Earned Income Tax Credit that claims a $3,000 refundable credit on a $2,000 tax liability gives you a $1000 tax refund.

- Nonrefundable credits: The credits may allow you to reduce your tax bill to zero, but not beyond that. If you owe a tax of 2,000 and have a nonrefundable credit of 3,000, you will owe no tax, but you will not get the remaining $1,000. However, the remaining part of the nonrefundable credits may be carried forward to the following tax years.

What are the typical tax deductions and tax credits?

Common Tax Deductions:

- Standard deduction: A fixed sum ($14, 600 when a person is single, $29, 200 when a married couple is filing as joint taxpayers in 2024), which is calculated against taxable income.

- Mortgage interest is the interest charged on home loans up to a specific limit.

- State and local taxes (SALT): Combined amounts of state income taxes and property taxes to the extent of $ 10,000.

- Charitable giving: Contributing to qualified non-profit organizations.

- Business expenses: Direct costs of doing business as self-employed.

- Student loan interest: Interest on education loans that are qualified to a maximum of $2500.

- Medical expense: Reimbursable medical expenses that are more than 7.5 percent of adjusted gross income.

- Retirement contributions: Mostly Traditional IRA and 401 (k) contributions.

Common Tax Credits:

- Child Tax Credit: A potential of up to $2,000 per eligible child below 17 years old is partially refundable.

- Earned Income Tax Credit (EITC): A refundable credit for low and middle-income working families.

- Child and Dependent Care Credit: A credit for the costs of caring for children so that parents can work.

- American Opportunity Tax Credit: It covers up to 2500 dollars per student on qualified education expenses.

- Lifetime Learning Credit: As much as 2,000 during the tax years on education and skill development.

- Retirement Savings Contributions Credit (Saver’s Credit): A tax credit to taxpayers with lower income who make contributions to retirement plans.

- Residential Energy Credits: Credits for solar panels and energy-efficient windows or other qualifying home improvements.

Conclusion

It is crucial to know the distinction between tax deductions and credits, yet to use the information in relation to your own case, it is necessary to involve professional skills. Our qualified tax accountants at H&M Tax Group, Dallas, TX, offer tax services in the filing of income tax to ensure that you receive all deductions and credits allowed to take maximum advantage of avoiding taxes without any violation.